The Income Tax Department has released the Draft Income Tax Rules, 2026, which are expected to apply from Financial Year 2026-27 after final approval. These proposed rules introduce significant revisions to several long-standing tax provisions, particularly those affecting salaried taxpayers and middle-class individuals.

Many commonly used allowances such as House Rent Allowance (HRA), Children’s Education Allowance, and Hostel Allowance are proposed to be revised for the first time in decades. If implemented, these changes could significantly reduce taxable income and overall tax liability for taxpayers who opt for the old tax regime.

The draft rules also propose updates to PAN quoting requirements for certain transactions, strengthening compliance measures.

Major Changes Proposed in Draft Income Tax Rules 2026

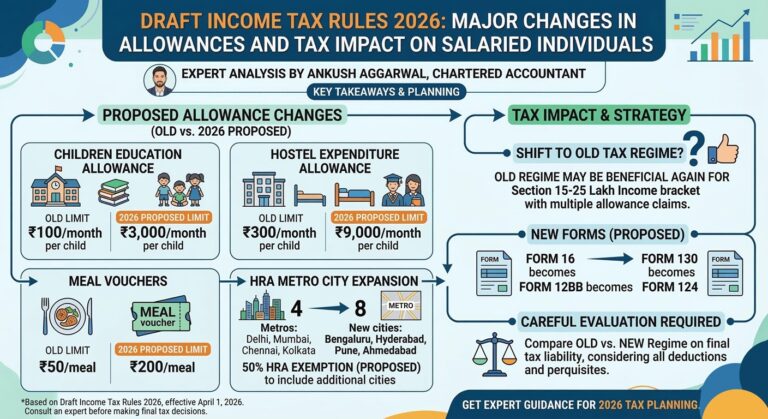

1. Increase in Children’s Education Allowance

Under the current Income Tax Act, 1961, the exemption available for children’s education allowance is:

- ₹100 per month per child

- Maximum of two children

The Draft Income Tax Rules 2026 propose increasing this limit to:

- ₹3,000 per month per child

- Applicable for up to two children

This increase reflects the significant rise in education costs over the years.

2. Increase in Hostel Expenditure Allowance

Currently, taxpayers can claim an exemption of:

- ₹300 per month per child

The proposed rules increase this allowance to:

- ₹9,000 per month per child

This revision acknowledges the rising cost of hostel accommodation and student living expenses.

3. Expansion of Cities Eligible for Higher HRA Exemption

The draft rules also propose expanding the list of cities eligible for higher HRA exemption. In addition to the existing metro cities such as Delhi, Mumbai, Chennai, and Kolkata, the following cities may be added:

- Bengaluru

- Hyderabad

- Pune

- Ahmedabad

Residents of these cities may qualify for higher HRA exemptions, thereby reducing their taxable income.

Tax Impact Example: Salaried Individual with ₹30 Lakh Salary

Consider a salaried employee earning ₹30 lakh annually. The gross salary remains the same across different tax regimes, but the taxable income changes significantly depending on exemptions and deductions available.

Assume the salary structure includes the following components:

- House Rent Allowance (HRA)

- Employer NPS contribution

- Children’s education allowance

- Hostel allowance

- Leave Travel Allowance (LTA)

- Food allowance

- Gift allowance

Comparison: Old Tax Regime vs Draft IT Rules 2026 vs New Tax Regime

*Note: Deductions are represented in parentheses to reflect accounting standards.

| Components (₹) | Old Tax Regime (Current 1961) | Old Tax Regime (Draft IT Rules 2026) | New Tax Regime (Revised Slabs) |

|---|---|---|---|

| PART A: Salary Components | |||

| Basic Salary + DA | 15,00,000 | 15,00,000 | 15,00,000 |

| House Rent Allowance (HRA) | 7,50,000 | 7,50,000 | 7,50,000 |

| Employer NPS Contribution | 1,50,000 | 1,50,000 | 2,10,000 |

| Child Education Allowance | 2,400 | 72,000 | 72,000 |

| Child Hostel Allowance | 7,200 | 2,16,000 | 2,16,000 |

| Leave Travel Allowance (LTA) | 50,000 | 50,000 | 50,000 |

| Food / Meal Allowance | 26,400 | 1,05,600 | 1,05,600 |

| Gift Allowance | 5,000 | 15,000 | 15,000 |

| Other / Special Allowances | 5,09,000 | 1,41,400 | 81,400 |

| Gross Salary | 30,00,000 | 30,00,000 | 30,00,000 |

| PART B: Exemptions Allowed | |||

| HRA Exemption | (6,00,000) | (7,50,000) | NA |

| Child Education Exemption | (2,400) | (72,000) | NA |

| Child Hostel Exemption | (7,200) | (2,16,000) | NA |

| LTA Exemption | (50,000) | (50,000) | NA |

| Food / Meal Exemption | (26,400) | (1,05,600) | NA |

| Gift Exemption | (5,000) | (15,000) | NA |

| Total Exemptions | (6,91,000) | (12,08,600) | 0 |

| PART C: Deductions Claimed | |||

| Standard Deduction | (50,000) | (50,000) | (75,000) |

| Section 80C | (1,50,000) | (1,50,000) | NA |

| Section 80CCD(1B) | (50,000) | (50,000) | NA |

| Section 80D | (25,000) | (25,000) | NA |

| Section 80CCD(2) | (1,50,000) | (1,50,000) | (2,10,000) |

| Total Deductions | (4,25,000) | (4,25,000) | (2,85,000) |

| PART D: Tax Calculation | |||

| Net Taxable Income | 18,84,000 | 13,66,400 | 27,15,000 |

| Base Tax Liability | 3,77,700 | 2,22,420 | 3,94,500 |

| Health & Education Cess (4%) | 15,108 | 8,897 | 15,780 |

| Total Tax Payable | 3,92,808 | 2,31,317 | 4,10,280 |

| Effective Tax Rate | 13.09% | 7.71% | 13.68% |

Key Takeaways

- The Draft Income Tax Rules 2026 significantly increase exemption limits.

- Total exemptions may increase from about ₹6.9 lakh to over ₹12 lakh.

- This could reduce tax liability substantially for salaried individuals.

- The new tax regime still provides greater flexibility and liquidity without the need to lock funds in investments.